Understanding Interest Rates and Fees on Credit Cards

Published 21 May 2025 · Updated 6 April 2026

Understanding Interest Rates and Fees on Credit Cards

The interest rate on a credit card is the most expensive form of borrowing most people will ever use. It is higher than a personal loan, higher than a mortgage, and higher than an overdraft. The standard purchase rate on a typical NZ credit card is well above what any other mainstream lending product charges. Understanding why — and how to avoid paying it — is fundamental to using credit cards sensibly.

How the Interest-Free Period Works

The headline feature of most credit cards is the interest-free period, typically up to 55 days on purchases. This is not a grace period on the entire balance from day one. It works backwards from your statement date. When you receive a statement showing a closing balance, you have until the due date — typically around three weeks later — to pay that balance in full. If you do, no interest is charged on any of the purchases on that statement.

The crucial detail is that the interest-free period applies only if you pay the full closing balance by the due date. Pay every cent except one, and interest applies to the full balance from the date of each transaction. There is no partial interest-free period. It is an all-or-nothing system. This catches a surprising number of cardholders who think paying most of the balance is good enough.

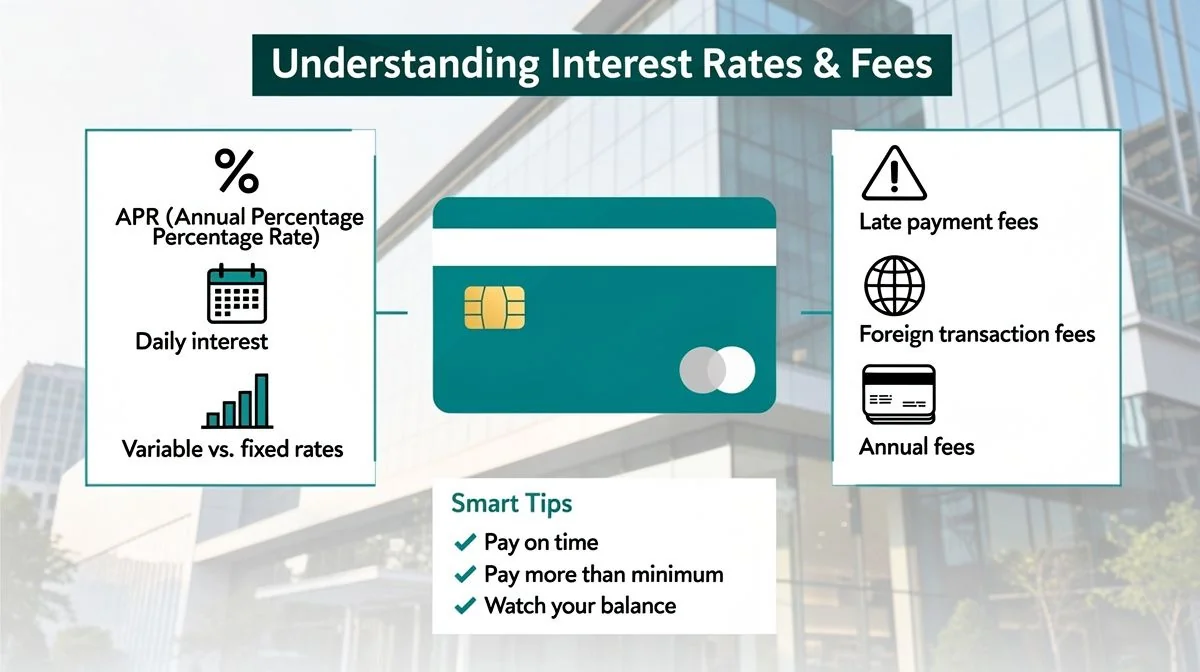

The Different Rate Types

Purchase rate is the rate that applies to everyday spending. This is the rate most people refer to when they talk about a card's interest rate.

Cash advance rate is higher than the purchase rate and applies to ATM withdrawals, cash equivalents like gambling transactions, and some types of money transfer. Crucially, cash advances have no interest-free period — interest starts accruing from the moment the transaction is processed. A NZ$200 cash withdrawal from a credit card will incur interest from day one even if the card is otherwise paid off in full every month.

Balance transfer rates are promotional rates offered when you move existing debt from another card. A typical offer might be zero percent for six months or a low rate for twelve months. The promotional rate applies only to the transferred balance. New purchases on the card are charged at the standard purchase rate. Payments are usually applied to the lowest-rate balance first, meaning the promotional balance is paid off last — a structure that maximises the interest the lender earns if you do not pay off the full amount.

Annual fees range from zero for basic cards up to several hundred dollars for premium cards with travel insurance and other benefits. A card with no annual fee but a high interest rate suits someone who pays in full every month. A card with an annual fee and a low interest rate suits someone who carries a balance. The trade-off between fee and rate is the central choice in card selection.

Late payment fees are charged when the minimum payment is not received by the due date. The fee is set by the lender and disclosed in the terms and conditions. A single late payment also ends your interest-free period, meaning all new purchases start accruing interest from the transaction date until the balance is paid in full.

The Real Cost of Carrying a Balance

Carrying a balance on a credit card compounds against you. Interest charged in one month is added to the balance, and the next month's interest is calculated on the higher amount. The effective annual rate, including compounding, is higher than the advertised monthly rate multiplied by twelve.

The minimum payment on most cards is a small percentage of the outstanding balance plus any fees and interest charged that month. Paying only the minimum each month means the balance declines slowly and the total interest paid over the life of the debt is substantial. On a NZ$3,000 balance at a typical rate, paying only the minimum each month takes several years to clear and costs a significant amount in interest.

The Difference Between Nominal and Effective Rates

Credit card interest rates are advertised as a nominal annual rate. The actual rate you pay, including monthly compounding, is the effective annual rate. The difference is not huge at the rates credit cards charge, but it exists. If the nominal rate is, say, around twenty percent, the effective rate with monthly compounding is a fraction higher. The important number is not the precise difference but the principle that compounding adds to the cost.

Understanding how interest accrues day to day is useful. Most card issuers calculate interest on the daily balance. Each day's balance is multiplied by the daily rate — the annual rate divided by 365 — and those daily amounts are added up at the end of the billing cycle. This means paying off a large purchase mid-cycle reduces the interest charged compared to waiting until the statement date to pay it. The earlier you pay, the fewer days of interest accrue.

Comparing Cards by Total Cost

The cheapest card is not the one with the lowest annual fee or the lowest interest rate in isolation. It is the card where the combination of fee, rate, and your personal spending behaviour produces the lowest total annual cost. A card with no annual fee and a high rate suits someone who pays in full every month. A card with a moderate annual fee and a low rate suits someone who carries a balance. A premium card with a high fee and included travel insurance suits someone who would buy that insurance separately anyway.

The annual fee divided by twelve gives the monthly cost of holding the card. Compare that against the monthly interest saving of a lower rate. If carrying a NZ$2,000 balance, a rate difference of several percent saves enough in annual interest to offset a moderate annual fee. For someone paying in full, a card with no annual fee and a high rate costs nothing in interest or fees, making it the cheapest option regardless of the headline rate.

The ValueHub Team built this site because finding clear, unbiased financial information in New Zealand was harder than it should be. Every guide is based on real research — we compare the actual fees, terms, and fine print so you don't have to. Our tip: shop around every year, read the policy docs, and never assume loyalty gets you the best deal.— The ValueHub Team

Try our Calculators

Use these free tools to crunch the numbers:

PAYE Calculator

Calculate your take-home pay after PAYE tax, ACC, KiwiSaver, and student loan deductions.

Compound Interest Calculator

See how your savings grow with compound interest over time. Free NZ compound interest calculator with yearly, monthly, and weekly compounding options.

Mortgage Repayment Calculator

Calculate your weekly, fortnightly, or monthly mortgage repayments. Free NZ mortgage calculator — try different rates, terms, and repayment frequencies.

Term Deposit Calculator

Calculate your term deposit returns before you lock in. Compare interest earned across different terms and rates with ValueHub's free calculator.

Savings Goal Calculator

Calculate how long it will take to reach your savings goal — and what monthly deposit you need to get there. Free NZ savings planner.

Credit Card Repayment Calculator

See how long it really takes to pay off your credit card — and how much interest you could save by paying more each month. Free NZ calculator.

Related Articles

Best Gold and Platinum Credit Cards in New Zealand

Best gold and platinum credit cards in NZ compared: when a $150 annual fee pays for itself through travel insurance and perks.

comparisonBest Personal Loans in New Zealand

Compare NZ personal loan rates: why major banks charge 12-14% while Harmoney offers 7.99% and how your credit score affects the rate you actually get.

comparisonBest Credit Cards in New Zealand

Compare the best credit cards in New Zealand for balance carriers and balance payers. Lowest rates, highest rewards, and the one rule that overrides everything.

guideWhen to See a Debt Recovery Lawyer in NZ

Know when to see a debt recovery lawyer in NZ, from debts over $30k to complex disputes and enforcement options.